Fed speakers repeatedly promise policy tightening is a story for next year or the year after. To quote Jerome Powell – “We’re not thinking about raising rates, we’re not even thinking about thinking about raising rates.”

Short term interest rates are approaching zero percent and will likely fall below zero shortly. The culprit is an unusual circumstance at the U.S. Treasury. As we discuss, the Fed may have no choice but to tighten monetary policy to offset the condition.

For investors banking on continuing massive stimulus, what unexpectedly lies ahead may not be the same as the road we have been traveling.

Buckle Up

Andreas Steno Larsen, of Nordea Bank, wrote a thoughtful article on a significant liquidity event on the horizon. His article, Brace Yourself… USD Liquidity is Coming discusses an interesting development with the U.S. Treasury’s cash account held at the Federal Reserve.

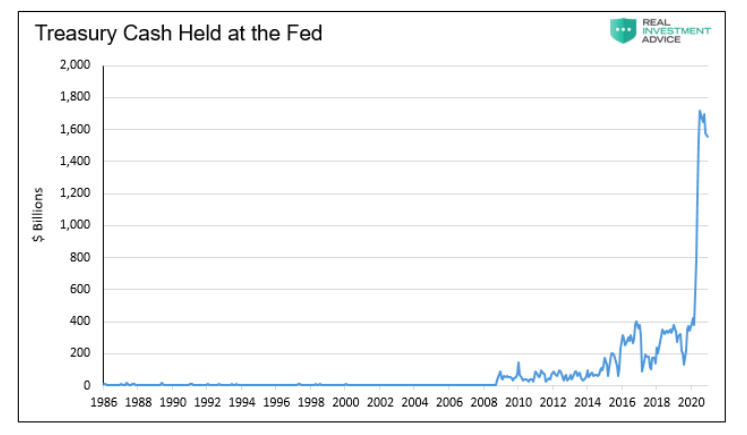

As shown below, the Treasury’s cash balance was never above $400 billion before the current period. Now it sits at four times prior record highs.

Over the last year, the Treasury borrowed massive sums of money to fund the CARES Act. It turns out they borrowed more than was spent. The extra cash now sits idle at the Federal Reserve.

In its February forecast, the Treasury estimates they will reduce its cash surplus to under $500 billion by the end of the second quarter.

Essentially they will spend down the cash to meet demands. As a result, their borrowing needs will be small over the period.

Per the U.S. Treasury (LINK):

During the January – March 2021 quarter, Treasury expects to borrow $274 billion in privately-held net marketable debt, assuming an end-of-March cash balance of $800 billion. The borrowing estimate is $853 billion lower than announced in November 2020.

During the April – June 2021 quarter, Treasury expects to borrow $95 billion in privately-held net marketable debt.

The Q2 borrowing forecast of $95 billion compares to $600 billion of debt issuance in the prior quarter and a total of $4.3 trillion for 2020.

Unintended Consequences

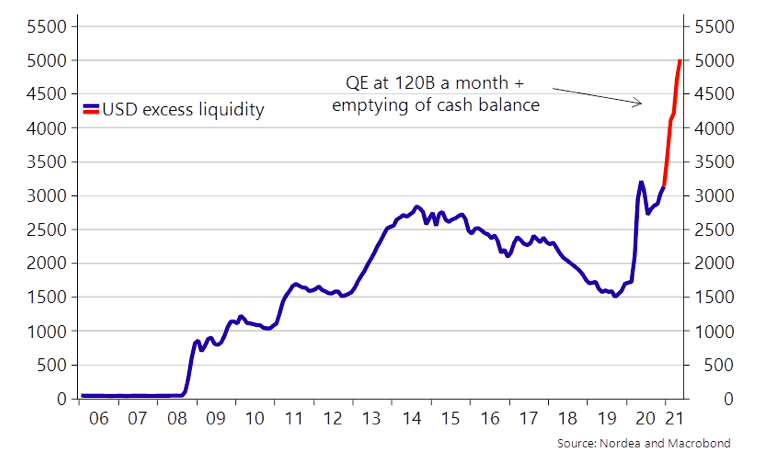

As noted, new issuance of Treasury debt will plummet as the Fed uses cash on hand. At the same time, the Fed vows to keep purchasing $80 billion of U.S. Treasury debt every month. The graph below, from Nordea, shows that excess liquidity (QE plus the trillion-dollar-plus reduction in cash balances) will rise substantially.

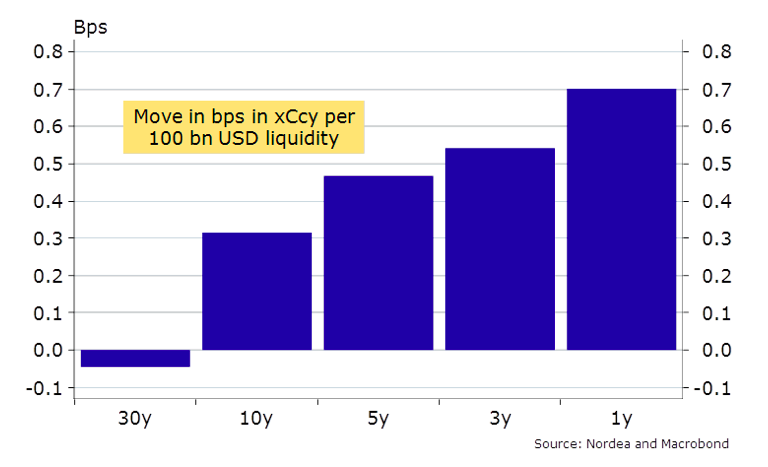

The most considerable effects will be felt in the shorter-term maturity sectors, which account for the most debt issuance. Short maturity debt remains in high demand as corporate and personal accounts have been demanding cash safety. The future supply reductions coupled with strong needs should result in lower yields. Further, the graph below, courtesy of Nordea’s article, shows increases in dollar liquidity are most correlated with shorter maturity yields.

Bottom line: short term interest rates are likely to go negative. That is unless the Fed takes action.

Fed Tightening

The Fed has been crystal clear they do not want negative rates. They prefer the Fed Funds rate to stay within its current target of 0.00-0.25%.

Below are four ways the Fed can drain liquidity in the money markets to offset the Treasury/Fed actions and try to keep rates positive:

– It can limit purchasing short term debt and instead favor longer-term bonds.

– They can take that a step further by selling short-term holdings and purchasing longer-term paper. Most recently employed in 2012, such an action is called Operation Twist. However, because it involves selling, the Fed must buy more than $80 billion a month in longer-term debt to meet its monthly goal.

– The Fed may use its reverse repurchase program (RRP) to remove liquidity. RRP, is a temporary swap of cash for securities. In this instance, the Fed would provide banks Treasury Bills in exchange for cash, effectively draining liquidity.

– A final tool in its toolbox is the interest the Fed pays banks on reserves (IOER). The current rate is .10%. The higher the rate, the more incentive for banks to sit on reserves and not lend them out. Reserves are the basis on which money is created. Therefore the Fed can prevent more cash from being created by keeping the IOER higher than similar money market investments.

Tightening

The four operations above, or anything else they dream up, reduce liquidity. Any reduction of liquidity is ipso facto tightening. If the Fed elects to keep short-term rates positive, how might other asset classes be affected?

Treasury Yields – Yield Curve Control

Yield curve control (YCC) is typically associated with central bank actions to cap long term interest rates. What we discuss above is the opposite. Essentially, the Fed would be setting a floor on short term rates.

YCC is the Fed’s attempt to shape the Treasury yield curve. Keeping short rates from going negative flattens the yield curve more than would otherwise be the case. If they employ either of the first two bullet points, aka Operation Twist, they will exert downward pressure on long-term yields.

The combination of reduced issuance of new debt and Fed operations, including buying more long term debt, should flatten the yield curve. However, we must caveat that prediction with current inflation concerns. Long term yields are rising in line with inflation expectations. Investors are balking at buying bonds with yields well below where they think inflation will be. Can Fed actions exert more influence than investors and push long-term yields lower?

How this tug of war ends, we do not know. We do know there will be a new bullish factor for long term bonds entering the equation.

U.S. Dollar

Unless the Fed is fine with negative rates, they must put a floor on money market rates. In such a case, cash depositors are somewhat assured rates will not decline further.

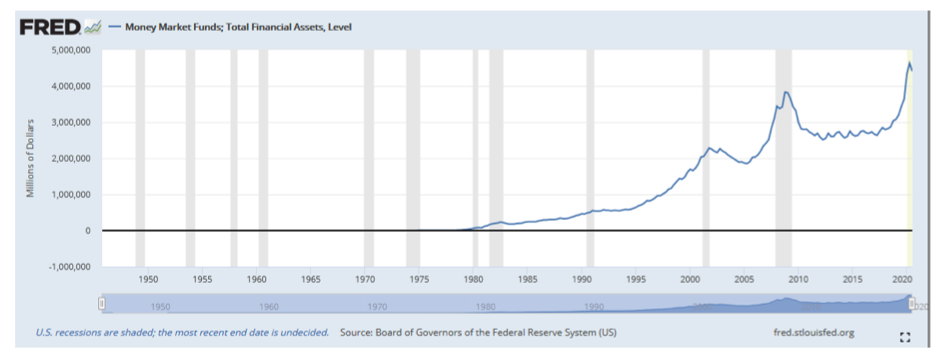

Across the pond, the Bank of England warned its banks to get ready for negative yields. They are likely to follow in the footsteps of the ECB and the BOJ with negative rates. As shown below, investors and corporations are sitting on a lot of cash.

That cash will flow to the safest place it can earn the highest yield.

Foreign investors electing to partake in higher U.S. money market yields must contend with currency risk. There is never a rate advantage when risks are appropriately hedged, using forward currency swaps and accounting for credit differences. In other words, forward currency rates reflect interest rate differentials. As such, if other countries further reduce money market rates and the Fed floors domestic rates, the U.S. dollar is likely to rise.

Equities

The question of what happens to stocks is not straightforward. A flood of liquidity is coming, but it appears the Fed will try to absorb it. It’s also unlikely money market investors, content with cash safety, will suddenly chase riskier assets even if yields decline further. Therefore the extra liquidity by itself may be a neutral influence on stock prices.

The recent weakening trend in the U.S. dollar is inflationary and a tailwind to higher stock prices. One concern is that a floor on U.S. rates, when global rates continue to go negative or more negative, should benefit the dollar. Any dollar strength will reduce said tailwind, possibly limiting more upside or even pressuring stocks lower.

Summary

The coming financial plumbing problems are just starting to percolate. The Treasury has no choice but to limit debt issuance and reduce its cash balances. The net result will be a wave of liquidity headed for the money markets. The Fed will need to tap on the brakes and at the same time keep its foot on the monetary stimulus pedal.

Event risk is rising. Asset markets may behave differently than they have as the Fed takes unusual actions. We urge caution as we are indeed in unprecedented times.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Rolling Over At Key Fibonacci Level?")