In my last article we looked at valuing a business using an asset valuation method. One of the issues identified was that intangible assets are not included, thereby giving a misleadingly low valuation of the company. Caterpillar (CAT) value their intangible assets on the balance sheet ($3,596m at 2013 YE) but if the intangible assets are not on the balance sheet, there are a couple of ways in which they can be valued.

Before looking at these, what are intangible assets? The most obvious of these are the Brands that an entity may possess, also, for example, Patents and Copyrights. These would form the intellectual capital of the company and are recognized as such by accounting standards. However, as with other assets, we have the issue of the historical cost convention and, in general terms, they are often understated. Intellectual capital also includes the workforce – for example, years of experience and accumulated skills. You can also include the data collected by the organisation and the knowledge accumulated over the entity’s existence. We can see therefore that in valuing a company we need to give intangible assets serious consideration. There are a couple of methods which we will look at now.

Valuation of Intangible Assets

The first method is very simple. We take the equity value of the company, either the market capitalization or a calculated version (we will look at these in future articles, dividend valuation model, discounted cash flow or P/E) and subtract the value of the tangible assets. If we look at CAT:

Market Capitalization (June 3rd 2014) $65,340.35m

Asset Valuation (2013 figures) $10,326m (see previous article, intangibles and goodwill removed)

Δ £55,014m

Looking at Caterpillar’s balance sheet we can see that intangible assets are valued at $3,596m (2013), providing a pretty good example of why this method is not always suitable.

The second method also has its issues but a brief description first may be of use. This is the calculated intangible value method. The first step is to calculate an industry average return on tangible assets and deduct this from the entity’s pre-tax profit. Hopefully this will give an excess annual return, from which we then calculate the post-tax value. The resulting figure is the calculated intangible value, which is assumed to continue in perpetuity. The entity’s cost of capital is used to calculate the perpetuity. We can use CAT (assuming for the moment that intangibles weren’t on the balance sheet) as an example, and compare to actual total asset value. This is by no means a perfect example but illustrates the process and will ensure consistency as we use CAT in this series of articles on valuation.

$(000)

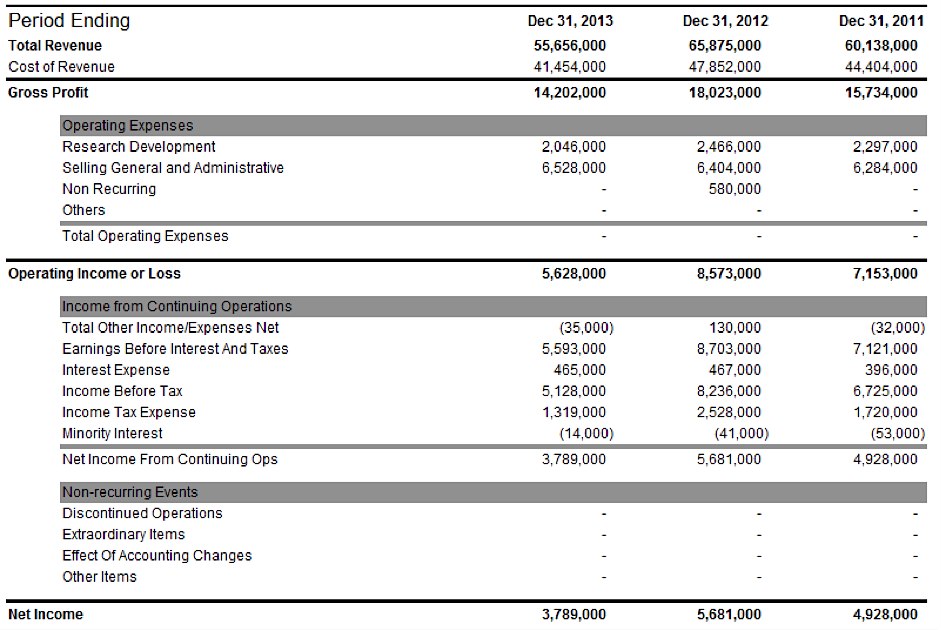

Pre-tax profit (Figure 1, below) 5,128,000

Industry Average ROA x Tangible Assets (4.15%1 x 74,344,000) (3,088,336)

Excess annual return 2,039,664

Post-tax (2,039,664 x 0.7289 2) 1,486,711

Calculated Intangible Value (assumed constant perpetuity3) 20,122,604

Total asset value: 20,122,604 + 74,344,000 94,466,604

In my previous article we saw that Caterpillar’s total asset value was £84,896,000 (including intangibles and goodwill). So this method adds an additional £10,000,000.

- Calculated by looking at Deere & Company (DE) and General Electric Company (GE)

- Effective tax rate approximately 27.11%

- WACC calculated to be 7.3883%

This method has a number of issues. Perhaps the most obvious is that arriving at an industry average return on tangible assets may not be a straightforward task. Pre-tax profit (not cash flow) is used, which is subject to accounting conventions and it is assumed that future intangible income growth will be constant at the company’s cost of capital. Essentially, this area of valuation must be approached with caution. In my next article, we will consider the most popular valuation method, the P/E valuation.

Figure 1: CAT Income Statement (sourced from Yahoo Finance)

Figure 1: CAT Income Statement (sourced from Yahoo Finance)

Thanks for reading.

No position in any of the mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.