Even if your focus is squarely on equities, understanding what’s taking place in other markets is an important factor when it comes to managing a portfolio. It’s often said that the bond market leads stocks and the first moves to a major change in trend, whether it’s the trend in markets or economy growth often begins with fixed income. And it’s fair to say that bond market concerns have been growing.

The Credit market has garnered much attention (at least in my opinion based on how much those I speak with have been talking about it) in the last 6-12 months.

One such piece of evidence around growing bond market concerns comes from Jeff Bahl, the former head fixed income trader at Goldman Sachs, who now manages his own fund. Bloomberg covers the story (h/t to Jesse Felder for sharing the story on Twitter).

I want to share a few points Jeff Bahl makes regarding credit, etc…:

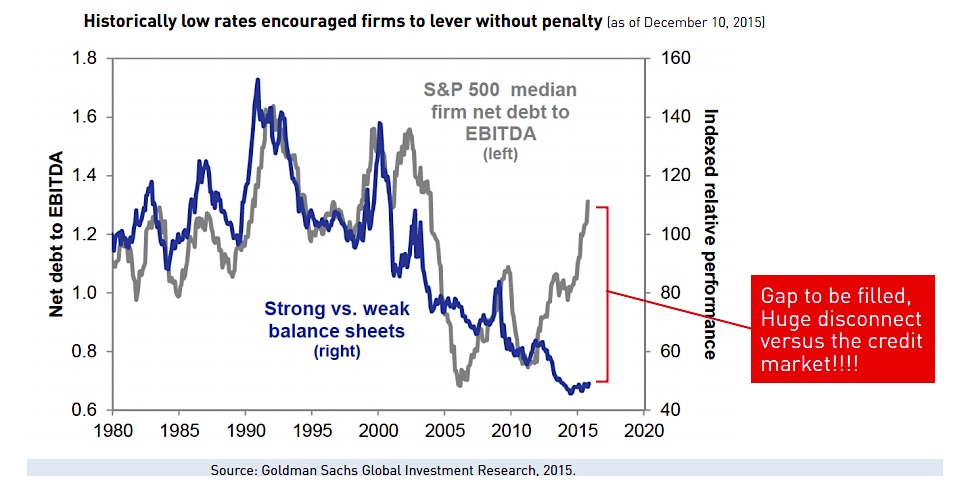

Historically, there has been a clear correlation between well-capitalized companies outperforming their weaker counterparts during periods of rising corporate leverage. However, that relationship has not held since 2011 as the market has rewarded higher leverage (indicated in the exhibit below). As a result of the positive feedback loop, debt on corporate balance sheets is now at levels not seen since the financial crisis.

Jeff Bahl makes a good point that ‘high yield’ bonds should not be categorized as such based on their credit rating, as history has shown credit agencies don’t always get things right. But that they should be viewed as ‘high yield…based on their actual yield (a novel idea!). He goes on to give two examples of this, with Freeport-McMoran and Sprint.

Bahl ends the letter with:

While history does not repeat, it certainly rhymes. This time it is not different. Corporations that have depended on the depth of the capital markets for their expansion are firmly in the crosshairs. As opposed to the past six years, a “V-shaped” recovery in credit spreads is not coming. Similar to the unwind of prior credit booms, this deleveraging cycle will be longer and deeper than market expectations. With a contracting credit market, further access to capital will be at progressively more punitive terms.

I’m not overly concerned about the “why” for the market, there’s plenty of opinion that can point you in a million different directions, any of which will surely fit your personal bias (whether it be crude oil, the dollar, China, or Donald Trump). What’s important in my view is understanding that the winds are changing in the fixed income and understanding the bond market concerns. There’s a hell of a lot more money at stake in credit markets, and when it moves it can have massive ripple effects.

The information contained in this article should not be construed as investment advice, research, or an offer to buy or sell securities. Everything written here is meant for educational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned.

Source: It’s What You Owe (Bahl & Goynor)

Twitter: @AndrewThrasher

Read more from Andrew on his Blog.

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Creating Bullish Divergence?")

: Creating Bullish Divergence?")