As the market rallied on Tuesday, there were plenty of upside alerts triggering. But one notable downside alert triggered as the Investment Grade Bonds ETF/Fund (LQD) broke below the $113 level. This was an interesting divergence from the market… and it occurred even as high yield bonds rallied.

I set this alert on the LQD back on December 29th, 2015 when the June 2016 $110 puts were bought to open in a large trade for 18,000 contracts at $1.65, a $2.97M position, and in an ETF that trades just 1,450 puts per day on average. This was clearly a flag for investment grade bonds.

On January 6th, 2016 the same June 2016 $110 puts were bought 13,250X at $1.55 to $1.60, and currently open interest stands above 33,500. LQD is a slow mover, but June Implied Volatility (IV) Skew is very steeply sloped and 30 day IV stands at a 2 year high, so the options market is seeing increasing amounts of risks to the fund… and this doesn’t bode well for investment grade bonds.

The top issuers in the LQD include Verizon (VZ), JP Morgan (JPM), Goldman Sachs (GS), Morgan Stanley (MS), Bank of America (BAC), Anheuser Busch (BUD), Wells Fargo (WFC), AT&T (T), Citigroup (C), and Microsoft (MSFT). In terms of exposure, Banking accounts for over 27% of the exposure, Consumer non-cyclical at 18.6%, Communications at 13.57% and Energy at 9.37% as the top four groups. The Investment Grade Bonds maturity are comprised as follows: 24.5% in the 3-5 year range, 17.4% in the 5-7 year range, 21.67% in the 7-10 year range, and 26.6% in the 20+ year maturity. In terms of credit quality just 1.99% are AAA rated, 9.97% AA Rated, 43.67% A Rated, and 43.8% BBB Rated.

The main risks to Investment Grade Bonds are slowing economic growth and a more aggressive Fed.

US corporate bonds started 2016 with the worst performance in 16 years and borrowing costs for investment-grade companies soared to a four year high in late January as Standard and Poor’s warned on the outlook for corporate borrowers. Morgan Stanley was out with a call on February 8th noting that Investment Grade Bonds are cheap and one of the few attractively valued, lower-beta investment opportunities in fixed income. Investment grade valuations have fallen to recessionary levels as credit risk has risen.

Not everyone agrees with Morgan Stanley as highlighted in the Wall Street Journal recently that Perry Capital, a $10B hedge fund, is making a $1B bet against investment grade corporate bonds.

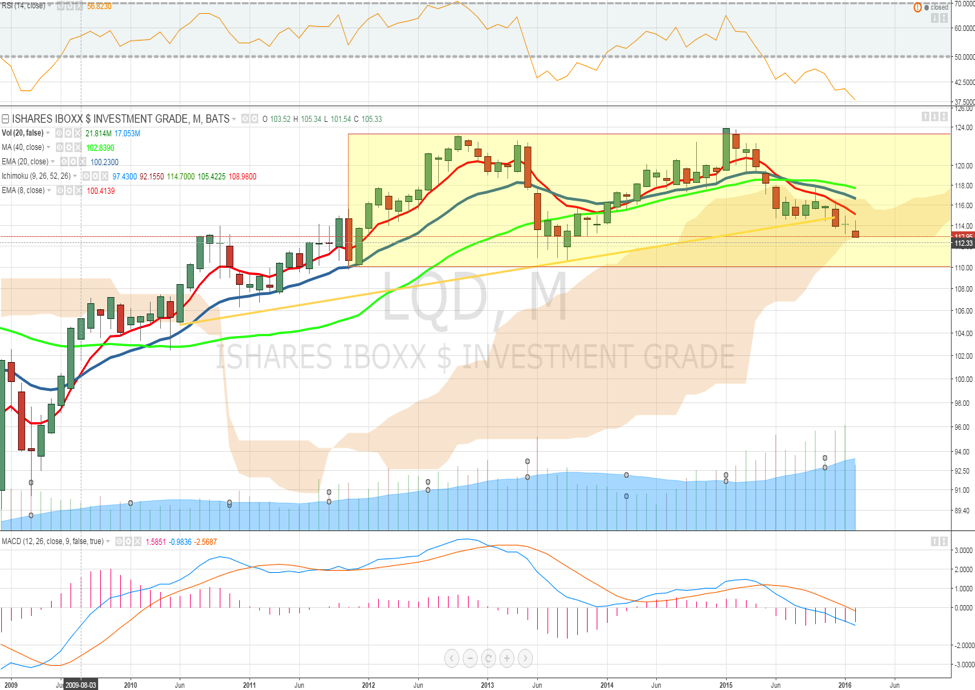

On the chart, LQD broke its 5 year uptrend back in December and is now breaking under its monthly IchoMoku Cloud. LQD also put in a major double top and the next key level is the $111 support from 2013 weakness, while a move below sets up for a longer term measured move down to $99. Monthly RSI has already broken down well below the 2013 level.

Thanks for reading.

Further reading from Joe: Options Traders Position For Return Of Market Volatility

Twitter: @OptionsHawk

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.