Solaris Oilfield Infrastructure (SOI) Stock Research & Outlook

Solaris is a $900M maker of mobile proppant management systems and provider of real-time inventory management solutions serving the oil & natural gas industries.

The company facilitates increased per well proppant consumption levels with innovative solutions and has a 15% market share in Mobile Proppant Management Systems. Its customers include Devon Energy, Apache & EOG Resources with most of its systems deployed in the Permian Basin.

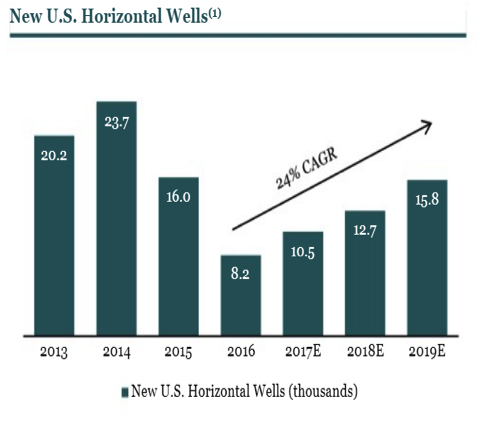

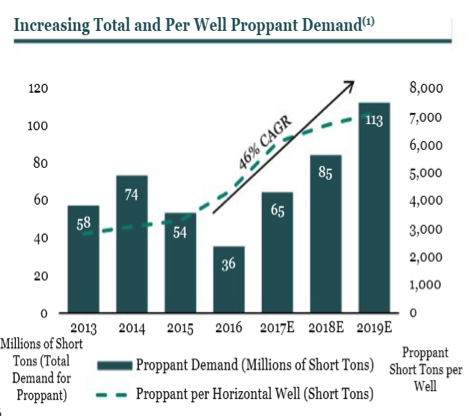

A recovery in oil prices is driving increased drilling activity and E&P companies are focused on higher recovery rates & returns. There is a clear trend of increased proppant usage and SOI’s solutions are a beneficiary. The company has expanded into transloading logistics with its new Kingfisher Facility that is targeting the STACK / SCOOP area.

The biggest challenges to the Oil & Gas industry currently are shortages with labor and trucking capacity, and SOI solutions improve efficiency of each of these.

Statistics source: Sentieo; images from company presentation.

Shares of SOI trade for less than 7X Earnings, 2.75X Book, 6.5X FY19 EBITDA and 4.2X FY19 EV/Sales with a balance sheet free of debt. The growth is very impressive generating 270% topline growth in 2017 and expecting 175% growth this year followed by another 50% growth in 2019.

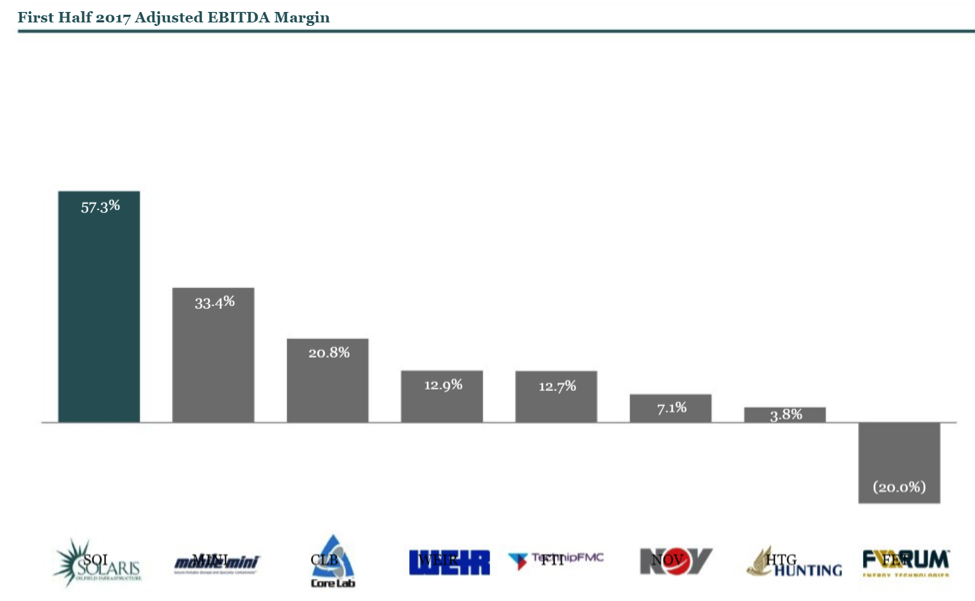

SOI continues to add systems to its fleet and is seeing strong revenue and EBITDA growth with an increase in revenue days. Its 57.3% adjusted EBITDA margins are well above all of its peers and its industry peers have an average 30.9% Debt/Market Cap, while SOI has zero debt. In Q1 SOI saw continued demand for its systems delivering 21 to the gleet and was virtually sold out the entire quarter, currently with 108 operating systems.

SOI has increased its number of customers by 33% this year and added 21% more systems to existing customers. SOI will be generating a lot of cash the next few years and will be looking at M&A to grow its platform, and may look at dividends & buybacks according to management.

CSFB has a $23 target and Outperform rating on shares citing the strong growth, utilization and demand for its products. SOI’s acquisition of rail logistics software integrated with its PropView system is intended to make it indispensable and sticky with customers. Gilder Gagnon Howe, Adage Capital, Times-Square Capital, and Victory Capital are all notable top holders of the name.

In closing, SOI is growing at an impressive rate while demand for its products is ramping. The company trades at a discounted valuation while having unheard of EBITDA margins, a clean balance sheet, and entering a period of strong cash flow generation. As long as Oil prices maintain at this level, it is a stock that can double over the next two years.

Check out more of my investing research and options trading ideas over at OptionsHawk. Thanks for reading and good luck out there!

Twitter: @OptionsHawk

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Flirting With Critical Support… Again")