Orchids Paper Products Co. (Ticker: TIS) is one of the more interesting stocks that showed up in a screen I designed looking for positive trends in EPS, Sales, and Gross Margins. The $313.3M maker of tissue products markets with brands such as Colortex, My Size, Velvet, Big Mopper, Soft & Fluffy, Linen Soft and Tackle. Orchids Paper Products sells its products at many of the discount stores like Dollar General (DG), Dollar Tree (DLTR), Wal-Mart (WMT), and Big-Lots (BIG).

Orchids Paper Products (TIS) shares trade 14.5X Earnings, 1.75X Sales, 2.35X Book and offers a 4.5% dividend yield. This micro cap growth stock has posted revenue growth of 15.4%, 22.6%, and 18% Y/Y since 2013 and expecting 15%+ growth in 2016/2017 as well. EPS is expected to hit $1.60 in 2016, up 16.8% Y/Y and doubling from $0.80 in 2011. Gross Margins declined in 2014/2015 to near 18% after being 22-24% in 2012-2013, and the Company forecasts a return to 21%+ margins in 2017.

In their latest quarterly report, Orchid Paper Products (TIS) beat EPS estimates by 86.7% and posted 27.5% Y/Y revenue growth. TIS saw margin improvements as converting costs lowered and fiber prices boosted results. One near-term headwind remains the Barnwell startup that has caused a rise in costs, but the paper machine is on schedule to start up in Q1 2017 and a second converting line in Q2 2016. The CEO mentioned on the recent earnings call a competitive environment due to promotional activity across higher brands, but sees a return to growth in the 2nd half, though Q2 could be bumpy.

Private-label tissue sales have a 5 year CAGR of +3.6% and continues to gain market shares over national brands, and TIS also is targeting regions seeing above-average population growth. Orchids Paper Products has just a 2% market shares of the At-Home Tissue market, compared to P&G (PG) at 27% and Kimberly Clark (KMB) at 16%, leaving a lot of room for growth via market share gains. Orchids has also been ramping up capacity at a 30% CAGR.

TIS only has coverage at 4 firms, an average price target of $34.50 with 3 Buy ratings.

Short interest has been climbing, now at 9.57% of its float, near a record high. Institutional ownership remains low under 45%, plenty of room for incremental buyers. Institutional ownership rose 4.6% in Q4.

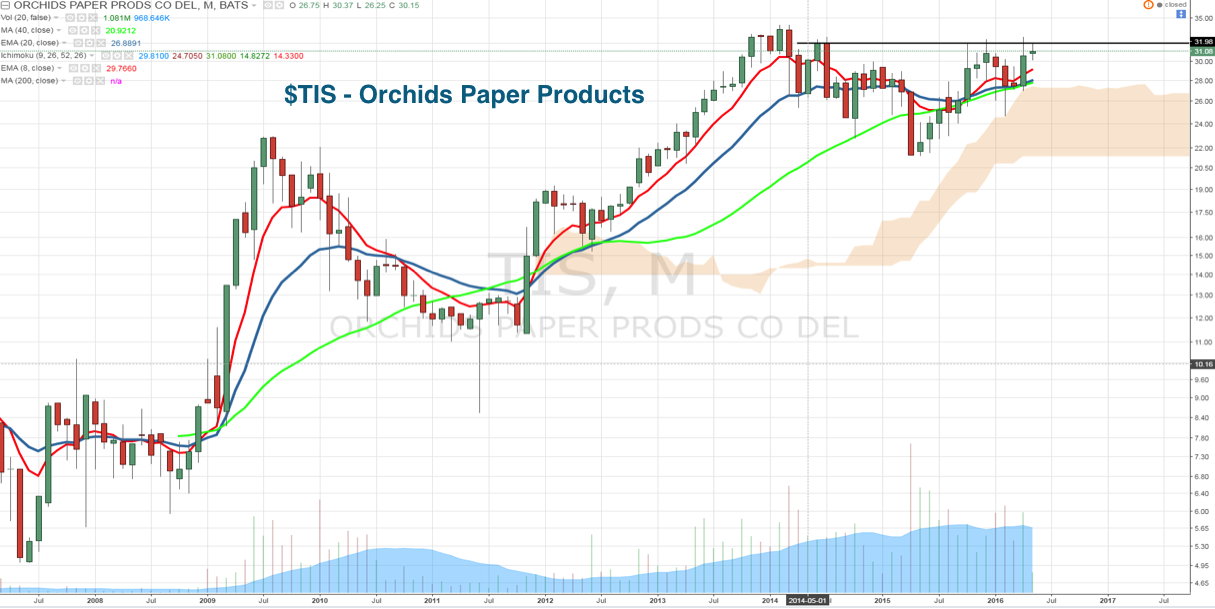

On the chart TIS shares are consolidating under the $32 level, looking to leave a range that can target a run to new highs at $40. The monthly chart is shown below. TIS also has a strong seasonality trend, shares averaging a 23% gain the last 5 years in Q4, far exceeding average returns in the other quarters (Q1 -0.22%, Q2 1.86%, Q3 -1.34%).

TIS is an attractive growth stock at a reasonable valuation that pays a strong dividend, and has plenty of available market to grow for years to come. One risk I see for the company is the merger between Family Dollar and Dollar Tree reducing the total store count, but I do not see a major overall impact on demand for its products. Based on the commentary and seasonality, I would look to buy this name after its next earnings report which could see some slowdown and knock the stock lower, but expect a very strong end of year as management has proved to be excellent operators. In the long term, if it continues to take market share as a private-label, it could attract a strategic buyer.

Thanks for reading.

Twitter: @OptionsHawk

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.