The S&P 500 (INDEXSP:.INX) and the NASDAQ Composite (INDEXNASDAQ:.IXIC) indices registered new record highs last week. Stocks found support from a steady flow of better-than-anticipated first-quarter earnings and economic reports suggesting business conditions are improving.

The expansion in corporate profits is most notable in large-cap multinational companies that are benefiting from a significant rebound in Europe’s economy.

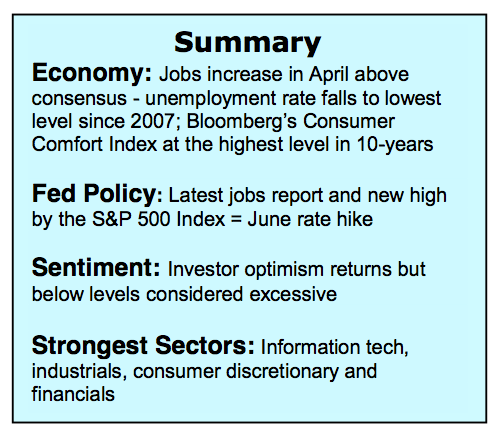

For the first time since 2014, forward earnings estimates are being adjusted higher. The April Employment Report issued last Friday showed job growth returning following the weak employment numbers in March. This offers credence to the view that first-quarter GDP was an anomaly and that the business environment is poised to improve. Federal Reserve Chief Janet Yellen suggested the disappointing first-quarter GDP number was ”transitory” in her remarks following the May meeting of the Federal Reserve’s Open Policy Committee. The fed futures market now gives June Fed rate hike a 100% probability on the heels of the lowest unemployment rate since 2007 and new highs by the stock market. Considering the outcome of the European election was in line with the consensus view and the likelihood that a June Fed rate hike is already baked into current prices, stocks are anticipated to attempt to add on to recent gains.

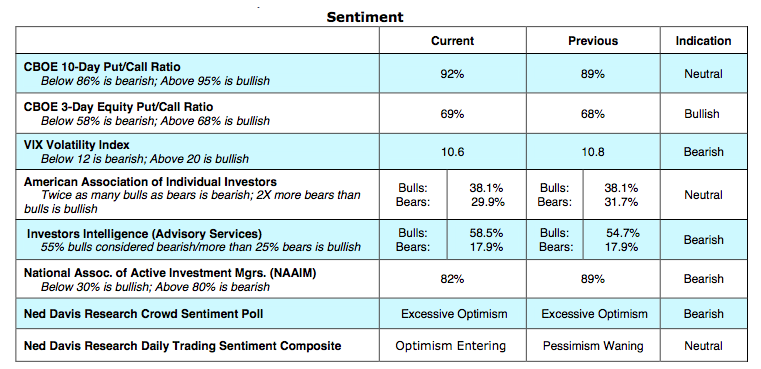

The technical indicators offer a mixed outlook for the stock market with the largest concern the quick return of investor optimism. The latest report from Investors Intelligence (II) which tracks the opinion of Wall Street letter writers shows a jump in bulls to 58% and only 17% bears. The most recent survey from the American Association of Individual investors (AAII) shows more bulls than bears for the second week in a row. The National Association of Active Investment Managers (NAAIM) now have an 82% allocation to stocks, indicating future buying power is likely limited.

The activity on the Chicago Board of Options Exchange (CBOE) offers a mixed picture. Demand is unusually high for equity options, which is interpreted as bullish for stocks but the CBOE’s Volatility Index at 10 suggests complacency is deeply seated. The most productive rallies the past several years have followed periods of excessive pessimism. The fact that this did not develop during the two-month consolidation period suggests the upside is limited near term. We would need to see a surge in market breath to include at least one session where upside volume exceeds downside volume by a ratio of 10-to-one or more. A bullish message from the broad market would relieve suspicions over sentiment and support the argument that a new leg up in the bull market is underway.

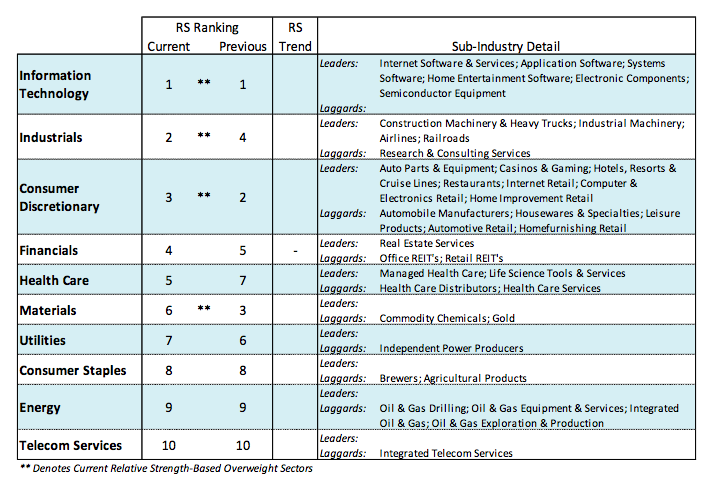

The strongest sectors remain those most closely tied to the domestic and global economies. This would include information technology, industrials, consumer discretionary and financials.

Thanks for reading.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

Ready To Break Out?")