By Max Moore Once in a while, I’ll poke fun at my Dad and his computer literacy skills. I look up to him and respect him as a businessman, father and mentor, but I just can’t resist poking a little fun at ‘Gen X’ when he asks me how to copy and paste.

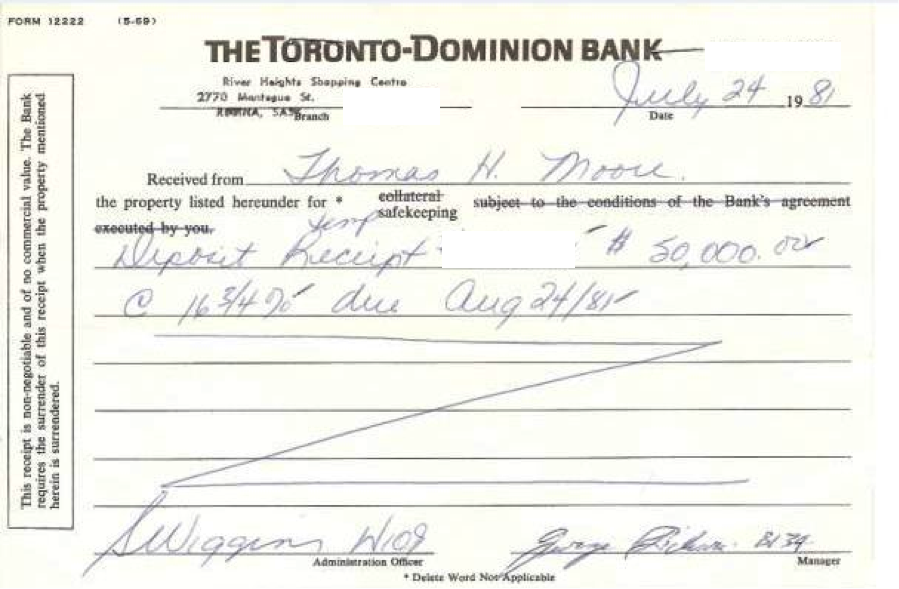

But, recently, he (and his sister) got back me. After clearing out some old Moore family storage boxes, they came across a GIC receipt (Guaranteed Investment Certificate) with a 16¾% interest rate. Quite the savings vehicle back then! Especially when compared with our ultra low interest rates environment (aka “ZIRP”).

The main reason I’m sharing this is because I came to the realization that you’re likely one of two types of people reading this: 1) someone that saw the 16¾% annualized interest rate and thought “I remember that,” or 2) someone that thought “Interest rates can go that high?!” Chances are you are Gen X and Gen Y respectively.

I’d known about the extremely high interest rates in the 1980’s, but seeing the receipt with my family name ‘Moore’ and ‘16¾%’ on the same page personalized it for me. It also made me realize that most of Generation Y has no idea what it’s like to earn interest on savings. The highest that bank interest rates have been at any point in my lifetime where I had enough money to put in the bank (in Canada) might be 3%-4%, and has spent much more of that time under 2%. In short, the incentive to save has not existed for much of the working lifespan of Generation X. This has lead to my generation seeing interest as an expense and not a source of revenue when it comes to personal finance.

On $50,000, 16¾% is about $698 in interest income per month. In 1981, that income would be enough to cover off the monthly rent for an average family home. While 16¾% was at or very near the highest interest rates that even Gen X had ever seen, earning even 5% on $50,000 at that time would have paid for the monthly lease on a decent vehicle (and put gas in it); or put a dent in tuition; or paid for monthly groceries and utilities. In today’s dollars, that $50,000 is about $100,000. With bank rates at 0.5%, saving $100,000 gets you about $42/month, or a nice lunch.

The message here is that the interest income earned on savings led to tangible benefits that made life and building wealth easier. I can’t help but wonder how much this dramatic, generational suppression in interest rates has fueled Gen Y’s intertemporal consumption habits (versus other demographic trends), and how long that might take to reverse. Thanks for reading.

Twitter: @maxmoore306 and @seeitmarket