The Uncivil Civil War discussed the sanguine approach many investors take towards equity risk despite clear signs of domestic political turbulence. The article put the upcoming elections and the growing political divisions amongst the populace into context with market risks.

While we read plenty of politically related articles and many more investment related articles, we have found precious few that bridge the gap and gauge the effect politics has on markets.

The intersection of markets and politics is important and should be followed closely, especially with a mid-term election months away.

As so eloquently described by the late Charles Krauthammer, “You can have the most advanced and efflorescent cultures. Get your politics wrong, however, and everything stands to be swept away. This is not ancient history. This is Germany 1933.”

In this article, we readdress politics and markets from an international perspective.

In particular, we focus on suspicions we have regarding Donald Trump’s negotiation tactics and goals for the U.S. relationship with Turkey.

Emerging Markets and the US Dollar

China, Turkey, and Iran are all classified as emerging markets. While the classification is broad and includes a diverse group of countries, these countries have many things in common. One is that their currencies, for the most part, are not liquid or highly valued. Thus, they heavily rely on the world’s reserve currency, the US dollar, to conduct international trade.

As an example, when Pakistan buys oil from Qatar, they transact in US dollars, not rupees or riyals. To facilitate trade efficiently, these countries must hold excess dollars in reserve. In almost all cases, emerging market nations rely on US dollar-denominated debt for their transactional needs.

Dollar-denominated debt is currently the cause of much economic pain for Turkey. To understand why, we present a simplified example. Suppose on January 1, 2018, a Turkish corporation borrowed $100 million US dollars with an agreement to pay it back with interest of 5% on August 15th, 2018. The company, as is typical, converts the loaned dollars to Turkish Lira. On August 15, 2018, the company will convert the Lira back to dollars in order to pay the principal and interest due on the loan.

The following graph charts the Turkish Lira versus the US Dollar over the life of the loan.

On January 1, 2018, one U.S. Dollar was worth 3.79 Lira. Over the next eight months, the US dollar appreciated significantly versus the Lira such that one US dollar was worth approximately 5.81 Lira. As such, the company will now need 5.81 Lira to purchase each dollar it needs to repay the loan. Due to the strengthening of the US dollar versus the Lira over the time period of the outstanding loan, the company would need 584,282,000 Lira to pay back what was originally a 378,750,000 Lira loan. In other words, the true all-in cost of borrowing was not 5% but 54%.

Turkey’s public and private sector dollar denominated loans outstanding are currently estimated to be around $500 billion. Turkish borrowers must grapple with repaying outstanding dollar-denominated loans by using more Lira to acquire the necessary dollars, and with the fact that interest rates, as set by Turkey’s central bank, have risen from 8% to 17.75%. To make matters even worse, the annualized rate of inflation is estimated to be over 100% in Turkey. Needless to say, dollar appreciation versus the Lira is bringing the Turkish economy to its knees.

Enter Donald Trump

Donald Trump, who authored a book entitled “The Art of the Deal,” takes great pride in his negotiating skills. Readers of this book know he highly values leverage in negotiations. As the President of the United States, Trump clearly has enormous leverage to change the global landscape. In the case of trade negotiations, we have seen repeated threats of tariffs against Mexico, Canada, Europe, and China. We believe the goal is to force these countries to renegotiate prior trade treaties or remove tariffs. For Trump, the leverage is the threat, which does the heavy lifting by forcing countries to negotiate or face still retaliatory tariffs or other penalties.

We suspect that Trump may also be using dollar appreciation to force nations, especially emerging markets, to comply with his demands. If you are looking for clues, consider the following Tweet from Donald Trump (8/16/2018): “Money is pouring into our cherished DOLLAR like rarely before.” Based on his bragging it seems Trump has few qualms about the recent strength of the U.S. dollar.

Regardless of the causes of the recent ascent of the U.S. dollar versus most other currencies, there is little doubt that Trump is using the dollar as a negotiating tactic to get what he wants.

There are a few reasons that Trump would manipulate the dollar, verbally or in actuality, to bring Turkey to the negotiating table. While we have no unique insight, the following reasons should be considered:

- Turkey opposes U.S. sanctions on Iran and vows to ignore them

- Turkey sits at a strategically important geographic intersection surrounded by Europe and Asia through which much east-to-west international trade passes

- If in a position to provide Turkey with a bailout, the administration can slow the growing de-dollarization trend

The bottom line is that it is likely that Trump is angling to sway Turkey towards stronger relationships with the U.S. in order to influence its relationship with China, Russia, and Iran. Keep in mind China’s One Belt One Road (OBOR) project, thought of as a new silk road, would provide increased economic competition and harm to America’s economic interests. China relies on Turkey’s participation to complete this project. As we put the finishing touches on this article, we also learned that Turkey, Iran, and Russia are in talks to schedule a trilateral summit.

Domestic Concerns

There is a healthy debate to be had about whether or not the US Dollar is being used as a negotiating lever. Since we may never know the answer, we focus on the potential outcomes if it is. If the US Dollar does strengthen further, how might it affect economic activity and assets?

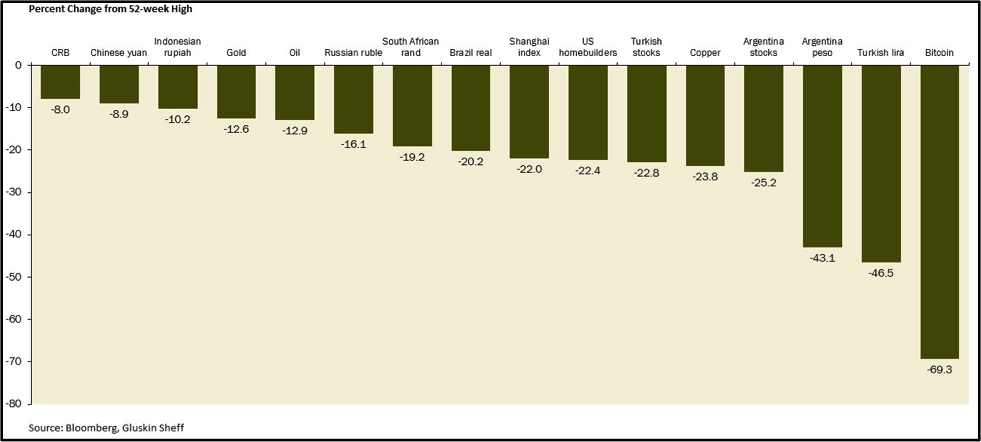

The following graph, courtesy David Rosenberg at Gluskin Sheff, shows the recent decline of many assets that are sensitive to the value of the US Dollar.

Of the assets above, only oil and U.S. homebuilders are having much effect on the U.S. economy or the performance of domestic investments. We think these losses will be broader-based globally and involve the US stock and bond markets if the dollar continues to appreciate. The following are potential domestic issues that could be brought about by further strengthening of the US Dollar:

- Deflation

- Worsening trade deficit, possibly prompting tougher sanctions and tariffs

- Reduced corporate earnings

- Contagion from a banking crisis in emerging markets spreading to domestic banks

When those and other economic headwinds become more evident, it is likely all markets will react. That reaction may move from asset class to asset class sequentially, as we are currently observing, or it may hit all assets at once in a sudden cascade of revaluation.

Summary

As we wrote this article, the U.S. stock market is showing some signs of weakness. Earnings-per-share forecasts for the S&P 500 have risen by 18% this year but the index is up only 6%. This might be an acknowledgment by investors of the international and domestic problems associated with dollar strength, or it may be something else entirely like liquidity constraints. If the market continues to stagnate as the dollar moves higher, we should turn our attention to the Administration for signs of rising concern over the value of the US dollar.

If in fact they do change their stance on the “cherished DOLLAR”, we would take this as a signal that either the domestic pain of a rising dollar has reached its threshold, or Turkey is acquiescing to U.S. demands. If the dollar fails to respond to verbal or direct manipulation, then it would be clear the market has another agenda and our concerns would be much graver.

For additional context on the role of the US Dollar in the global economy, we recommend our prior article Triffin Warned Us.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.