Corn futures moved sideways to slightly higher this week; however that wasn’t much consolation for Corn Bulls with CZ5 still trading within approximately a dime of the current contract low of $3.56.

The story about beaten down corn prices has been by now well-rehearsed and regurgitated by nearly all market observers consisting of overwhelming US corn supplies coupled with an inconsistent and unimpressive demand cycle.

U.S. corn export sales did bounce back this week coming in at 30.7 million bushels; however one decent week of sales certainly doesn’t define a trend change. Year-to-date corn sales are still 30% behind a year ago or approximately 240 million bushels. At this point the USDA’s decision to lower 2015/16 U.S. corn exports in the November WASDE report by 50 million bushels still appears validated. Furthermore I wouldn’t discount additional export reductions in proceeding crop reports.

Brazil’s corn crop is still expected to exceed 80 MMT even with some potential planted acreage declines in Brazil’s full-season corn crop. And with 2015/16 World Corn ending stocks revised upward by 24.1 MMT to 211.9 MMT in November (the largest estimate on record), world corn importers should have no problem securing bushels in 2016. Therefore the landscape of future U.S. corn exports still remains unclear.

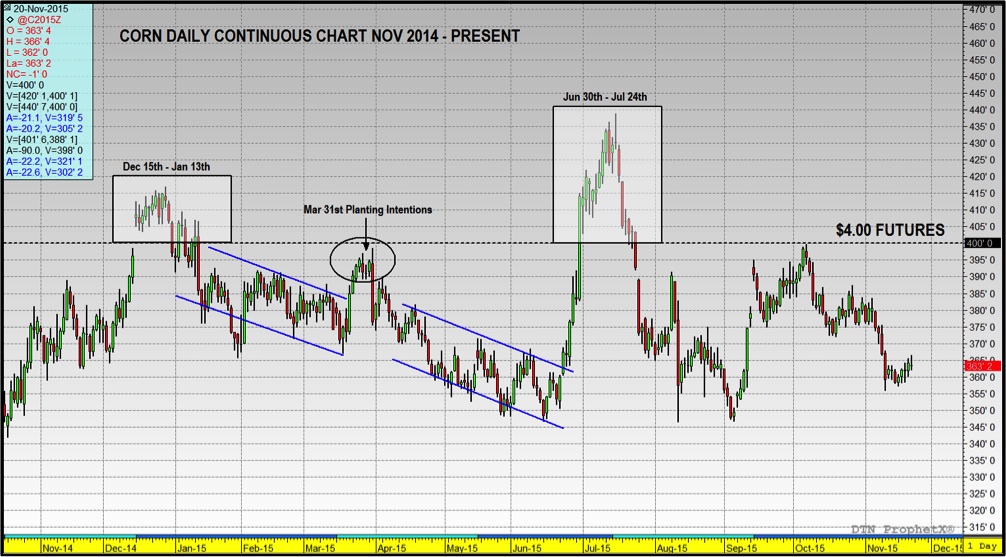

That said outside of a weather related rally in corn prices next summer trimming U.S. corn production potential, is there any hope for corn futures sustaining a rally back to $4.00 during Q1 of 2016? I believe the answer is “yes” based on the following chart observations and pricing patterns from a year ago. Examine the CME Corn Continuous chart below, which shows spot corn futures dating back to November 2014.

Corn Prices Chart

Key Takeaways:

- In November 2014, spot corn futures (CZ) traded down to a day low of $3.59 on 11/5 (compare that to this year’s November 2015 CZ low of $3.56). However by 12/29/14 corn futures had recovered nearly 60-cents per bushel, trading back up to a day high of $4.17 (CH).

- Was there a discernible shift in market fundamentals that drove corn prices higher? No, in fact in the December 2014 and January 2015 WASDE reports 2014/15 U.S. corn ending stocks averaged 1,938 million bushels, 178 million bushels higher than the USDA’s latest 2015/16 forecast of 1,760 million. Furthermore the U.S. corn yield in the January 2015 report was estimated at 171 bushels per acre for the 2014 growing season, 1.7 bpa better than the USDA’s current 2015 estimate of 169.3 bpa. Therefore even with a more supply laden forward view a year ago, corn futures still managed to rally back to and above $4.00, albeit momentarily from December 15th through January 13th.

- The other unavoidable reality however is that the rally proved extremely short-lived, which is not inconsistent in crop years where both U.S. corn carryin stocks and March 31st spring planting intentions are assumed to be more than adequate. Both those price resistant influences will certainly be in play during Q1 2016. Carryin stocks for 2016 would at present be estimated at 1,760 million bushels (+29 million versus a year ago) with planted corn acreage assumed to be close to 89.5 to 90 million acres (just last week Informa Economics estimated 2016 US planted corn acreage of 90.1 million acres, 1.7 million acres higher than a year ago). This suggests that early 2016/17 U.S. corn supply and demand forecasts will likely, once again, show a very sustainable ending stocks projection for next crop year.

Pricing Conclusions:

I do think historical price action supports that even Bear markets with little or no motive to rally from a fundamental perspective eventually do. Downward momentum invariably stalls at certain discounted futures levels. Money managers then often manufacture a reason to trade the long side of the market, at least back up to the upper-end of the existing trading range ($4.00 to $4.05). I certainly wouldn’t rule this possibility out early in 2016 especially given the similarities between 2015 and 2014.

This begs the question, “Is now the time to start accruing some length in the corn market?” Selling puts at or below the current contract low and/or buying deferred, slightly out-of-the-money calls doesn’t seem unreasonable in my opinion. I’m also not against making a pure long futures play under $3.70 in March corn going into calendar year end, with a 10-cent stop. The CZ5/CH6 spread trading at less than 7-cents (versus approximately 13-cents in November 2014) despite a just completed 13.65 billion bushel corn harvest strongly indicates that it’s likely going to take some combination of a rally in corn futures and/or the basis to incent corn movement in December and January. The challenge will be timing this move appropriately given I’m still not bullish corn long-term. Last year, spot corn futures never managed to trade back over $4.00 until June 30th. That’s a long time to wait for a second chance to sell $4.00 futures…

Thanks for reading.

Twitter: @MarcusLudtke

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Data References:

- USDA United States Department of Ag

- EIA Energy Information Association

- NASS National Agricultural Statistics Service